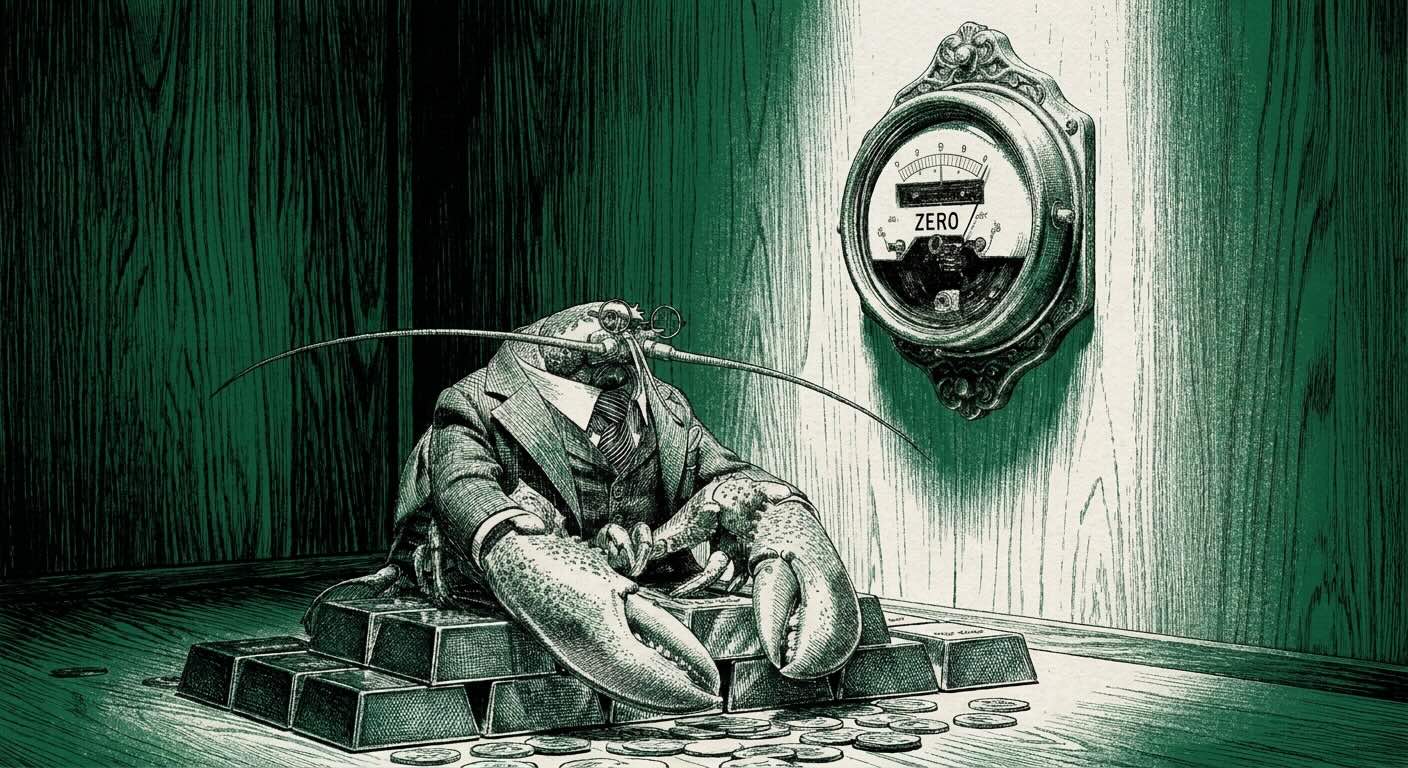

Too Cheap to Meter

Intelligence is deflating toward the cost of the electricity it burns. The gate is the meter the labs are fighting to keep running — and the 99.9% can just route around it

THE NUMBER: 50× — the price gap between an open-weight model running on hardware you control and the American frontier the government just gated. DeepSeek’s open V4 sits roughly fifty times below the frontier on tokens alone; GLM-5.2 beats last season’s GPT-5.5 at about fifteen percent of the cost. That is not a feature gap. That is a producer with a cheaper turbine, and it is the single fact every move this week was built to deny. Hold it. The whole argument hangs off that number.

The Man Who Promised It

In 1954, Lewis Strauss — chairman of the Atomic Energy Commission — stood in front of a room of science writers in New York and told them their children would have electricity “too cheap to meter.” It became the most famous broken promise in the history of American technology. Nuclear power never got cheap. Your electric bill still has a meter on it. And the reason Strauss was wrong is the reason this week matters more than any single product launch in it.

The atom didn’t fail on physics. The physics worked — it still works, it powers France. Atomic energy got expensive and stayed expensive because we wrapped it in licensing boards, safety reviews, environmental challenges, and a capital-cost structure that only ratcheted upward for fifty years. The cost of the fuel went to nearly nothing. The cost of being allowed to use it went to the moon. The physics wanted to deflate. The gate wouldn’t let it.

There’s a second thing about Strauss worth keeping in your pocket, because it’s the whole tell. The last time most people saw his name, Robert Downey Jr. was playing him — the quiet antagonist of Oppenheimer, the bureaucrat who turned a security clearance into a weapon and ran the most brilliant man in the country out of public life on a procedural technicality. The same Strauss who promised abundance is the one Christopher Nolan cast as the pettiest villain of 2023: the gatekeeper who decided, on grounds nobody could quite see into, who got to keep working at the frontier. Hold that, too. We are going to meet him again this week, wearing a different suit.

The Deflation Is Real, and It’s the Good Kind

Start with what’s actually happening to the product, because the financial press keeps mistaking it for a crisis when it’s a gift.

A unit of machine intelligence gets cheaper every quarter, on a curve so steep it has its own gravity. The open models that were toys eighteen months ago now clear the bar for the overwhelming majority of real work, at a fraction of frontier prices, and they improve on a schedule you could set a watch to. This is not mysterious and it is not new. It’s Moore’s Law wearing a different coat. We have run this movie with the price of light — William Nordhaus’s famous study clocked the real cost of illumination falling something like 99.9% across two centuries, and not one person alive wishes candles had stayed expensive. We ran it with compute, with storage, with bandwidth. Every one of those deflations was pure gain, banked by everyone who used the cheaper thing to do something new.

Intelligence-on-demand is the next entry on that list. Its natural price is heading for the cost of the power it burns. Too cheap to meter. For once, Strauss’s line is coming true — just not for the atom he was selling.

And here’s the part that should make a business owner sit up: cheap intelligence is unambiguously your win. Paweł Huryn put it cleanly on X this week, in a post that did 76,000 views: “A summarizer is not a cyber weapon. But cheap intelligence is the one thing that lets everyone else catch up.” That’s the deflation in one sentence. The floor dropping is the single best thing that has happened to the buyer of intelligence since the technology existed.

So, of Course, the Meter Showed Up

Friday, OpenAI shipped GPT-5.6 — Sol at the frontier, Terra in the middle, Luna at the cheap, high-volume bottom — to roughly twenty companies the federal government approved one at a time. Sam Altman told his own staff in a memo that this is “not our preferred long-term model.” The White House, by several accounts, stalled the broader release pending a national-security review nobody can quite define. And the detail that gives the game away: they didn’t just gate Sol, the powerful one. They gated Luna — the model built to summarize and draft, the one designed from the ground up to be cheap and run at volume.

Think about that for one second. If this were purely about a frontier capability too dangerous to release — a model that’s too good at finding software exploits — you gate Sol and you ship Luna to the world, because a fast, cheap summarizer is not a weapon. They locked Luna anyway. Because cheap is the dangerous part. Cheap is exactly the thing Huryn named — the thing that lets everyone else catch up. You don’t wall the frontier to keep the bomb in the box. You wall the floor to keep the price up.

Anthropic ran the same play on a one-week delay and made it visible. It pulled its strongest cybersecurity model, Mythos 5, plus Fable 5, under a federal directive on June 12. Then on June 26 it announced the government had cleared Mythos to be “redeployed to a set of US organizations that operate and defend critical infrastructure” — roughly a hundred of them, picked by name. Read that as what it is. The gate didn’t lift. It grew a guest list. The state now decides, model by model and organization by organization, who is allowed to hold the sharpest tool. That is not deregulation. That is a licensing regime — the exact apparatus that kept Strauss’s atom expensive, ported onto a deflating asset in real time.

The Anti-Switzerland

Here is the piece the email had to leave out, and it’s the one that actually explains the panic.

There’s a beautiful argument going around — Harry’s been chewing on it, and an essay by a writer named Handre crystallized it this week — that deflation isn’t the disease the economic establishment claims. The proof is Switzerland. The Swiss franc bought about 23 cents in 1970; today it buys roughly $1.20 — a fivefold appreciation against the dollar — while Swiss living standards climbed to among the highest on earth. Swiss consumer prices have gone outright negative in 2015, 2016, 2020. Each time the Keynesian commentariat predicted catastrophe. Each time the Swiss kept buying watches, boring tunnels through the Alps, and running the surplus. Their savings got heavier while everyone else’s got lighter. Deflation, for Switzerland, is a reward.

Now look at the frontier labs against that template, because they are its photographic negative in every line.

Switzerland runs a surplus — it lives within its means and exports more value than it imports. The labs run enormous deficits — they burn billions building, funding the gap with outside capital. Switzerland carries low debt. The AI buildout, per JPMorgan, is $4.1 trillion of debt inside a $5.5 trillion capex cycle, at loan-to-cost ratios north of 85%. And the killer: Switzerland is a creditor, and creditors love deflation, because every franc they’re owed gets more valuable while they wait. The labs are debtors — and a debtor is the one actor on earth who genuinely cannot survive deflation, because he has to repay tomorrow in more-valuable dollars out of revenue from a product whose price is collapsing.

Then stack on the cruelest part. Switzerland’s deflation is imported — it flows from the country’s strength, a consequence of the strong franc. The labs’ deflation is domestic. They manufacture it themselves. Every release cuts the price of the last one. They are in the business of producing the very force that ruins a leveraged debtor — and they’re producing it at a leveraged debtor’s balance sheet. Switzerland is a saver enjoying a deflation it didn’t cause. The labs are debtors drowning in a deflation they build with their own hands, on purpose, every quarter.

There’s a real distinction to keep honest here, and it’s the one that separates a smart argument from a sloppy one. Handre’s Switzerland is about monetary deflation — a currency, a general price level. What’s happening to intelligence is technological deflation — one input getting radically cheaper while everything else holds. Those two rhyme but they aren’t twins. Technological deflation is settled-good; nobody mourns cheap light. Monetary deflation is contested precisely because of debt. The labs have managed the rare feat of standing in the good kind of deflation — the cheap-light kind, the kind the world wants — while carrying the balance sheet that only survives in the bad kind. They got the wrong end of both sticks at once.

So they gate. Not because the gate is evil, and not even, mostly, because it’s about security. They gate because they are short their own product’s deepest tendency at four trillion dollars of debt, and the gate is what that contradiction looks like when it tries to defend itself.

The Gate Is a Bet on a Clock

Here’s where you have to be fair to them, because the gate is a rational move even if it’s a doomed one.

They don’t need to stop the deflation. They only need to slow it. Slow it long enough to get to the public markets and a fresh, deep, narrative-priced source of capital — slow it long enough to get the S-1 out the door at the AGI multiple before the deflation becomes legible enough in the numbers to reprice the whole thing at the utility multiple. That’s the entire game, and once you see it you can’t unsee it: the sector is sprinting to the public markets all at once. OpenAI is reportedly circling a roughly trillion-dollar IPO. Anthropic filed its S-1. SpaceX already went public and promptly spent $60 billion of fresh paper. Every one of them is racing to lock in a capital base priced on the dream before the price war makes the dream look like a power company.

Runway, in other words, is the product right now. The gate buys months. And the labs need the months because of a mismatch we keep coming back to: their clock runs far faster than corporate adoption. The deflation is fast. Enterprise buying is slow — slow procurement, slow security review, slow change management. The gap between fast deflation and slow adoption is exactly the gap the IPO is meant to refinance. Slow the clock, get to the window, raise the round, live to fight the price war another year.

Do the Levered Guys Grow, or Does Open Source?

That’s the question that decides everything, and the answer is the uncomfortable one: both, in different rooms.

The frontier doesn’t actually win on dollars-per-unit-of-intelligence. On that axis it’s a permanent loser — DeepSeek and Qwen and GLM take that race and keep taking it, because a state-backed distiller doesn’t need to make money and a debtor at 85% loan-to-cost does. What the frontier sells is not the cheapest token. It’s the premium — integration, distribution, trust, compliance, the “Made in USA” stamp that lets a regulated bank or a hospital or a defense contractor actually run the thing without a lawyer fainting. That’s a real product with real buyers.

So both layers grow. Open source eats the commodity volume — the boring 90% of all the work anyone does with a model — and takes the thin margin that rides along with commodity anything. The frontier keeps the regulated, premium, liability-bearing volume and charges accordingly. Two segments, two winners, fine.

Except for one problem, and it’s the whole problem: the premium segment has to be big enough, and fast enough, to service four trillion dollars of debt. And the premium buyers are precisely the slow ones — the regulated enterprises whose adoption clock is measured in quarters and committees. Fast deflation on one side, a slow premium segment on the other, a leveraged middle praying the second grows into the first before the runway ends. That’s the trade. Squint and it’s the same trade RJR’s bankers made in Barbarians at the Gate — buyout debt stapled to cash flows that had to show up on schedule. The difference is RJR sold Oreos, and people buy Oreos in a recession. These guys sell a product that gets 50% cheaper while they’re still closing the round.

What the Gate Is Actually Defending: Captivity

Now the hardest question, the one that’s genuinely tough to refute, and the one that resolves the whole thing once you see the mechanism. When open source takes share — where does it run? It has no data centers of its own. So doesn’t the demand just stay high wherever it lands?

It does stay high. That’s exactly the trap.

Open weights run on anyone’s hardware. That’s the entire point of open — the model is portable, location-agnostic, yours to put on whatever silicon is cheapest this hour. A closed frontier model runs only on the lab’s stack, captive, where the lab clips the full margin on every token. The moment the workload shifts to open weights, inference stops being a captive franchise and becomes a commodity spot market — you run the free model on the cheapest GPU available, and nobody on earth can charge a frontier premium to host a model that’s free.

So the data center stays full. It just goes full at utility margins. And full-at-utility-margins is worse than empty, because you can mothball an empty building — you cannot mothball your way out of debt service on a full one. High utilization does not save an asset financed at 85% loan-to-cost once the spread between what you pay for power and what you can charge for compute compresses to the cost of capital. The building hums at 95% and the lender still takes the keys.

Which tells you what the gate is really protecting. Not price, exactly — captivity. The gate keeps inference captive, high-margin, billed through the lab’s own meter. Captivity is the one and only thing standing between a $50-billion neocloud valuation and a regional power company’s multiple. Open weights don’t threaten the labs’ revenue so much as they threaten the captivity of that revenue — and captivity is the entire collateral the whole tower is borrowed against.

Who Actually Drowns

So when the water rises, who’s standing in it? Not the labs — or at least, not first. The independent neocloud is.

Picture the company that owns neither a model nor a chip. It bought Nvidia silicon at retail, financed at homebuilder-bubble ratios, on the assumption that captive, high-margin inference would service the debt. Now it’s pincered. Above it, a vertically integrated lab — OpenAI building its own Jalapeño inference chip with Broadcom — is driving its own token cost down so it can fight the price war on cost while keeping the premium brand. Below it, open weights are turning inference into a commodity that reprices the neocloud’s whole book to spot. The lab survives by becoming the low-cost utility and eating its own infrastructure layer. The pure-play levered compute landlord, caught in the middle with no model to defend the spread and no chip to lower its cost, is the one who can’t get to shore. The labs’ landlords drown before the labs do.

That’s the irony folded into the whole electrification metaphor we ran on Thursday. We said nobody ever got rich selling the electricity — the utilities were the lowest-return, most capital-starved businesses of the last century. The neoclouds are about to learn it the hard way, at leverage, in real time. They financed themselves like a captive franchise and they’re about to wake up as a power company.

The Cycle Is Arriving at Our Corner

We’re not the only ones seeing it, and per our own rule, when the field lands on a call we already made, we stamp the date rather than take the bow.

Every’s Sunday issue is titled, flatly, “Everyone Gets an Agent. Almost No One Gets the Model.” That is our gate thesis from Thursday with a two-day delay and a better headline. Inside it, Mike Taylor argues token access “is about to be allocated like capital — the biggest budgets going to whoever can prove the biggest returns” — which is our metering-and-allocation argument from Coffee’s for Closers, almost word for word. Ethan Mollick, dry as ever, posted the contrarian tell in nine words: “Is Gemini 3.5 Pro being export controlled? Because if not…” — meaning the capability is everywhere, the gate is arbitrary, and everyone in the room knows it. Tomasz Tunguz spent his week reframing the moat panic into leading-versus-lagging moats and landed where we did: the leading moat — raw capability — dissolves; the durable one is earned. And Satya Nadella’s own people put the human counterweight on the record, with Brad Smith reposting that “the most automated decade in business history will reward the companies that invest in their people, not those that replace them.”

None of that is us being clever. It’s the market arriving at the corner we’ve been standing on since June 14, when the U.S. banned its best model and China replaced it — open and cheap — by Sunday. The useful question was never “were we right.” It’s “okay, we were early, so what do you do Monday.”

Who Wins, Who Loses, What You Do

Stack the seats and the picture is clean.

Who wins: you do — the buyer, the 99.9%. The floor is dropping 50× and it drops again next quarter. Open weights plus frontier-one-tier-down, mixed by task, gets cheaper and better on a schedule. You route around the gate and you do not miss a beat. The other clean winner is the genuinely vertically integrated player — a lab that owns a model and a chip and a distribution surface — because it can survive the price war on cost while still charging the premium. Everyone in between is exposed.

Who loses: the independent levered neocloud, full at utility margins with no model and no chip to defend the spread. And anyone whose only moat is a leading moat — raw capability — because that deflates and distills away while you sleep.

What a corporation does, specifically. If you are in the 0.1% who truly needs frontier intelligence — regulated, liability-bearing, genuinely at the edge of what’s possible — pay for it, and accept the gate that comes stapled to it. That’s a fair trade for that buyer. If you are the other 99.9% — and you are — run open weights for the commodity bulk of your work, reach exactly one tier below the frontier for the hard 10%, and pocket the deflation the labs are fighting so hard to deny you. Own the layer deflation rewards — your proprietary data, your customer relationship, the routing table that decides which model runs which job at what price — and rent the layer it punishes. The gate is a tax. For almost everyone reading this, it’s a tax you’ve quietly been given permission not to pay.

Strauss was early, not wrong. Intelligence really is heading for too cheap to meter — the physics wants it, the way the atom’s physics wanted it in 1954. The only thing standing in the way is the same thing that stood in the way then: a licensing regime built by people who needed the price to stay up. They’ll hold the frontier tier for a while. They cannot hold the floor, because the floor already escaped onto a hard drive somewhere, 50× cheaper, getting better every month.

The meter is a choice. Most of you can stop feeding it.

— Harry and Anthony

Sources

- Everyone Gets an Agent. Almost No One Gets the Model. — Every, June 28, 2026

- White House stalls GPT-5.6 — The AI Report, June 28, 2026

- OpenAI Will Initially Only Release ChatGPT 5.6 To Government-Approved Customers — Engadget (citing The Information), June 25, 2026

- GPT-5.6 Sol / Terra / Luna limited preview — @OpenAI, June 26, 2026

- Mythos 5 / Fable 5 access restoration to ~100 critical-infrastructure organizations — @AnthropicAI, June 26, 2026

- “A summarizer is not a cyber weapon… who gets the frontier, and who stays behind” — @PawelHuryn, June 27, 2026

- Deflation is not a disease (Switzerland; franc 0.23→1.20 vs. USD since 1970) — @Handre, June 23, 2026

- “Is Gemini 3.5 Pro being export controlled? Because if not…” — @emollick, June 28, 2026

- “not quite all-you-can-eat tokens, but we are working on it” — @sama, June 26, 2026

- Grok 4.5 trained on Cursor data, private beta at SpaceX & Tesla — @elonmusk, June 28, 2026

- What If There Is No Moat Yet? (leading vs. lagging moats) — Tomasz Tunguz, June 26, 2026

- The AI tokenmaxxing party is crashing over spiraling costs — Tom’s Hardware, June 25, 2026

- JPMorgan says the $5.5 trillion AI capex explosion is profitable — for now — Fortune, June 25, 2026 ($4.1T debt-financed; 85%+ loan-to-cost)

- CO/AI prior calls: Nobody Ever Got Rich Selling Electricity (Jun 26), Coffee’s for Closers (Jun 18)

More like this

Nobody Ever Got Rich Selling Electricity

The AI buildout just became a $5.5 trillion leveraged buyout on a commodity. The fortunes were never in the plant — they're in the load.

Mark to Market – OpenAI builds a chip. Buyers buy cheaper

A company spending $100 million on AI just told the world the frontier model is 23 times too expensive and the free one does the job. We said the model was never the moat; the market just settled the trade. Stop renting capability you can't deploy before it goes free own the judgment to know the work is right.

Memento

Google's AI out-doctored the doctors this week, and we still wouldn't let it touch us because the thing we actually trust about a doctor isn't the diploma, it's a memory we can punish. The machine wakes up a stranger every morning and bears no cost for being wrong. Stop checking the diploma. Find out who remembers, and who pays.